The app revolution has changed the way software is distributed and used among consumers. With a perfect storm of digital distribution, free content and powerful touch screen devices, the success of mobile apps has disrupted industries from telecommunications and games to music and news. To date, no category of apps has been more successful than Games, directly disrupting the traditional gaming industry. Flurry recently wrote about the impact iOS and Android game popularity has had on Sony and Nintendo. And with low barriers to entry for armies of entrepreneurial developers, indie game developers continue to thrive on iOS and Android.

Consider for a moment Facebook’s speedy billion-dollar acquisition of Instagram, a service that succeeds by delivering Facebook’s core value proposition of photo sharing, but only on mobile. When one understands that consumers now spend more time in mobile apps than they do online, Instagram’s value begins to make sense. With over 500 million iOS and Android devices in the market, mobile apps are the new battleground for consumer engagement. If Facebook feels compelled to snap up Instagram in this way, perhaps this is an indication of how relevant social networking has become in mobile apps, or simply how relevant mobile has become overall. In this report, Flurry focuses on the rise of the Social Networking category in mobile apps. Let’s start by looking at where consumers spend their time by application category.

In the chart above, Flurry compares the time consumers spend across different application categories when using smartphones. Starting on the left, we look at the average number of minutes a consumer spent each day, over the course of Q1 2011, across different app categories. For this period, we calculated that consumers spent 25 minutes (37%) of their app-using time in Games. They additionally spent 15 minutes (22%) of their time in Social Networking apps. News and Entertainment were the next most popular categories, garnering an average of 11 (16%) and 10 (15%) minutes per day, respectively. All other categories combined made up the final 7 minutes (10%) of time. During Q1 2011, Flurry tracked approximately 30 billion application sessions worldwide.

On the right, we conduct the same analysis for Q1 2012. Compared to the same quarter in 2011, time spent per consumer each day increased from 68 to 77 minutes. Additionally, the distribution of time spent per category shifted. Games usage dropped by 4% down to 24 minutes per day, while Social Networking increased by 60% up to 24 minutes per day. Games and Social Networking categories each controlled 31% of consumers’ time. News, Entertainment and Other categories commanded 12 (15%), 10 (13%) and 7 (9%) minutes, respectively. Flurry tracked approximately 110 billion application sessions during Q1 2012.

The most significant trend is that, for the first time in the history of applications (Flurry began tracking application usage in 2008), another app category is rivaling Games. We take the rise in Social Networking apps as a signal of maturation for the platform. As game demand may be hitting its saturation point, consumers are also discovering other apps, namely Social Networking. The year-over-year growth in Social Networking has been staggering. Not only has time spent increased by 60%, but also within a growing amount of total time spent in smartphone apps among consumers, from 68 to 77 minutes, or a growth rate of 13%.

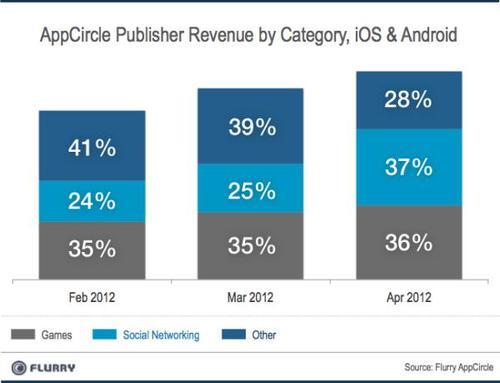

Through its mobile app traffic acquisition network, Flurry AppCircle, the company can also see how apps with growing audiences earn revenue through advertising. When app developers amass larger audiences, among the chief ways to monetize their businesses is by showing ads to their consumers. In the chart below, we show revenue earned by publishers in the Flurry AppCircle ad network for each of the last three months. Flurry AppCircle reaches over 300 million unique devices per month, making it one of the industry’s largest ad networks by reach. The columns in the chart grow from month-to-month at the same proportion as AppCircle publisher revenue growth. From just February to April of this year, Flurry AppCircle publisher revenue has grown by 23%. Please note that we forecast the remaining few days of April for the chart below.

From inspection, ad revenue in apps is driven primarily by Games and Social Networking categories. In other words, audiences using these apps a combination of the largest and most receptive to ads. For February, March and April, Games apps earned 35%, 35% and 36% of total ad revenue in the AppCircle network. Over the same three months, Social Networking climbed from 24% in February to 25% in March, and then to 37% in April. This is the first time in Flurry’s history that any category has surpassed Games in ad revenue generated (Flurry launched AppCircle summer 2010).

Over the last couple of years, the term “SoLoMo” was coined to describe the convergence of social experiences on mobile devices that leverage some element of proximity (i.e., location) to the experience. While a Silicon Valley term in origin, it speaks to the new consumer experiences possible when dreaming up any combination of these three factors. Phones are powerful, connected and always with consumers. And they are considered personal devices that easily enable sharing of personal content and information through apps. Build a clever app that leverages these aspects in a compelling way, and you could have the next Pinterest or Instagram.

As business ventures, the ability for Social Networking apps to engage consumers in a meaningful way is driving a wave of investment and bullish valuations. Social networks like Pinterest, Path and Skout are raising major venture capital rounds. This month, Andreessen Horowitz invested $22 million into Skout, and Greylock and Redpoint helped plow $30 million into Path. Pinterest, which has a strong mobile component, has become the third most popular social network behind Facebook and Twitter, and ahead of LinkedIn, Tagged and Google+. With so much innovation, coupled with high engagement among consumers, this appears to be only the beginning.

The rise of Social Networking apps also signals the end of the era of gaming dominance within mobile apps. While the free-to-play business model performs extremely well, enabled by in-app-purchases, it does so primarily for simulation games, a sub-genre of the total games category. As long as the total iOS and Android installed base grows, all categories will continue to grow naturally. However, as we reach saturation for mobile gaming on a per user basis (one consumer can play only so many free-to-play games), the Games category could start behaving more like a “zero sum game” from here on out, meaning that game companies would have to fight over a finite group of consumers in order to grow their businesses. For one app to grow, it would have to take from its competitors. Even with an influx of new consumers into the market, the expected would-be casual gamers will be increasingly wooed away from games by compelling Social Networking and other apps. Going forward, the Games category will have to look to innovate on mobile to maintain its dominance and growth.

For the comparison of minutes spent in this blog post, it’s important to clarify that these figures exclude tablet usage, and focus on smartphones only. While Flurry calculates that consumers spend an average of 94 minutes per day using mobile apps, that figure is a reflection of total usage spread over both smartphones and tablets. When we isolate just smartphone usage, as we’ve done in this analysis, the number of minutes spent on apps is lower.